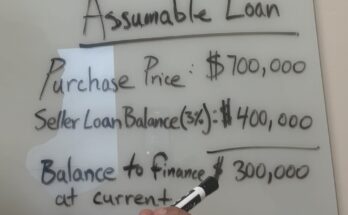

Assumable Loans – Yesterday’s Rates Today

Are Assumable Loans an option?

Read More

HONEST | TRUSTWORTHY | PROFESSIONAL | KNOWLEDGEABLE | BILINGUAL

Are Assumable Loans an option?

Read MoreI read an interesting article this morning about first time home buyers and financing. The article highlighted some of the friendlier low down payment loan products offered by many large …

Read More